$4450

$3560

[Research Report] The bioprocess technology market size was valued at US$ 30,897.49 million in 2022 and is projected to reach US$ 77,090.05 million by 2028; it is estimated to register a CAGR of 16.8% from 2023 to 2028.

Analyst’s Viewpoint

The advantages of bioprocess are using lower pressure, lower temperatures, and more conducive pH levels, and the entire process is renewable. Growing R&D spendings to introduce new drug compounds and increasing prevalence of chronic diseases. Stringent regulatory policies are the most impacting factors responsible for influential growth of the bioprocess technology market. Additionally, introducing advanced bioprocess technologies provide lucrative market opportunity for the overall market to grow exponentially during the forecast period. Further, emergence of Automated Real?Time Flow Cytometry (ART?FCM) acts as a future trend for the market to grow during 2023–2028. According to the segmentation profiled in the report, based on type segment, cell culture media bioprocess accounts a largest share; likewise, chromatography bioprocess is anticipated to register the highest CAGR during the forecast period (2023–2028). Furthermore, by modality, the single-use segment will account considerable share for the bioprocess technology during the forecast period. In terms of end user, the biopharmaceutical companies’ segment will dominate the bioprocess technology market growth during the forecast period.

Bioprocess technology is a critical part of biotechnology that deals with processes combining living matter or its components with nutrients that produce specialty chemicals, reagents, and biotherapeutics. Different stages associated with bioprocess technology involve substrates and media preparation, biocatalyst selection and optimization, volume production, downstream processing, purification, and final processing. Bioprocess technology is widely used, from food and pharmaceuticals to fuel and chemicals.

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Bioprocess Technology Market: Strategic Insights

Market Size Value in US$ 30,897.49 million in 2022 Market Size Value by US$ 77,090.05 million by 2028 Growth rate CAGR of 16.8% from 2023 to 2028 Forecast Period 2023-2028 Base Year 2022

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Speak to Analyst

Customize Research To Suit Your Requirement

We can optimize and tailor the analysis and scope which is unmet through our standard offerings. This flexibility will help you gain the exact information needed for your business planning and decision making.

Bioprocess Technology Market: Strategic Insights

| Market Size Value in | US$ 30,897.49 million in 2022 |

| Market Size Value by | US$ 77,090.05 million by 2028 |

| Growth rate | CAGR of 16.8% from 2023 to 2028 |

| Forecast Period | 2023-2028 |

| Base Year | 2022 |

Mrinal

Have a question?

Mrinal will walk you through a 15-minute call to present the report’s content and answer all queries if you have any.

Speak to Analyst

Market Insights

Growing R&D Spendings to Introduce New Drug Compounds

Pharmaceutical companies are spending huge sum in R&D to introduce new molecules with enhanced medical and commercial potency for various therapeutic applications. In the fiscal year 2019/2020, 16 pharmaceutical companies made it to the list of the world’s Top 50 companies in terms of total R&D investment. Novartis, Roche, Johnson & Johnson, Merck & Co, GlaxoSmithKline, and Pfizer are among the world’s Top 10 companies with high R&D investments.

R&D Investments by Major Pharmaceutical Companies

Company | R&D Investment in 2022 (US$ Million) | R&D Investment in 2021 (US$ Million) |

Gilead Sciences Inc | 27,305 | 27,281 |

Bristol-Myers Squibb Co | 46,159 | 46,385 |

Amgen Inc. | 26,323 | 25,979 |

Pfizer | 100,330 | 81,288 |

Merck & Co | 59,283 | 48,704 |

AbbVie Inc | 58,054 | 56,197 |

Note: The currency conversion rates have been considered wherever required.

Source: Annual Reports of Companies and The Insight Partners Analysis

The patent expiry of blockbuster molecules, a limited number of potential products in the pipeline, and the increasing demand for biologics have driven companies to adopt novel technologies, such as single-use bioprocessing technologies, in order to facilitate a quick cost-effective turnaround process for products. Single-use component and system manufacturers typically produce and assemble products in clean rooms to ensure they do not introduce harmful particulates and endotoxins into a bioprocess. Thus, high investments in R&D are made to introduce new drug compounds and aid in the development of bioprocessing technologies; these technologies support emerging biomanufacturing capabilities and related interoperability of raw materials, bioreactors, and unit operations.

Type-Based Insights

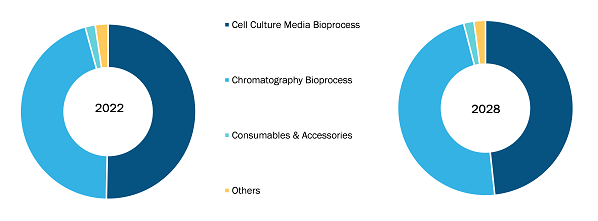

Based on type, the bioprocess technology market is segmented into cell culture media bioprocess, chromatography bioprocess, consumables & accessories, and others. The cell culture media bioprocess segment held a largest market share of bioprocess technology in 2022 whereas chromatography bioprocess is anticipated to register a highest CAGR during the forecast period (2023–2028).

Modality-Based Insights

Based on modality, the global bioprocess technology market is bifurcated into single use and multiple use. The single use segment accounted a larger market share for bioprocess technology in 2022. The multiple use segment is expected to grow at a higher CAGR during the forecast period.

End User-Based Insights

In terms of end user, the bioprocess technology market is categorized into academic & medical institutions, biopharmaceutical companies, research laboratories, and others. The biopharmaceutical companies segment held a largest market share in 2022, whereas academic & medical institutions is expected to register a higher CAGR during the forecast period.

Regional Analysis

North America dominated the bioprocess technology market accounting maximum share. The bioprocess technology market growth in this region is attributed due to the presence of large players launching innovative products (particularly related to bioprocess technology), growing product introduction in the region, and technological advancements in bioprocess technology. In North America, the US records maximum share for the bioprocess technology. According to the Food and Drug Administration (FDA) report, over 30 million people in the US suffer from ~7,000 rare diseases, accounting for life-threatening conditions with low treatment options. Drug, biological, and device development in the treatment of rare diseases is challenging due to a lack of understanding of the history of rare diseases and difficulty in conducting clinical trials. Therefore, the growth of bioprocess technologies such as gene and cell therapies (CGTs) and specialty pharmaceuticals represent a radical shift in the treatment of rare diseases. For example, CGTs have revealed significant health benefits than formulated drugs for treating rare diseases. In the US, more than 900 investigational new drug (IND) applications targeting gene therapy products are underway. Also, 10-20 gene therapies are approved annually by the FDA. Likewise, in August 2022, the FDA approved Bluebird Bio's "Zynteglo (betibeglogene autotemcel)." It was the most expensive single-application drug approval in the US intended for the treatment of a rare neurological disorder—cerebral adrenoleukodystrophy (CALD).

Likewise, Asia Pacific region will account highest CAGR for the bioprocess technology market. Among Asia Pacific region, China will hold considerable market share for the bioprocess technology market. The bioprocessing capacity globally has increased at an average of 12% since the past decade, as per the BioPlan Associates Top 1000 Biofacility Index and Biomanufacturers Database report. China is well positioned as a global participant in markets with both small and large-molecule drugs, accounting for second and third position, respectively, worldwide. Also, China is home to several developers of cell and gene therapy due to China's base for contract development and manufacturing organizations (CDMOs), accounting for ~25% of the country's bioproduction capacity. Therefore, China has considerable biomanufacturing capabilities but strict adherence to the global GMP standards that build confidence in the biologics' safety and effectiveness.

Country | Biomanufacturing Facility (L) | Global Capacity (%) | Estimated Capacity CAGR (%) |

China | 1.77 million | 10.2 | 15-20 |

Source: Global comparison of biomanufacturing capacity; data from the BioPlan Associates Top 1000 Biofacility Index and Biomanufacturers Database (CAGR = compound annual growth rate).

Bioprocess Technology Market Report Scope

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc, Corning Inc, STAMM Biotech, Lonza Group AG, Eppendorf SE, Repligen Corp, Danaher Corp, and BioPharma Dynamics Ltd are among the leading players operating in the global bioprocess technology market growth. Several other essential market players were analyzed for a holistic view of the market and its ecosystem. The report provides detailed market insights, which help the key players strategize their market growth. A few developments are mentioned below:

- In June 2022, Merck has entered a collaboration with Agilent Technologies to advance Process Analytical Technologies (PAT). PAT, which is strongly encouraged by global regulatory authorities, is a key enabler for real-time release and Bioprocessing 4.0.

- In March 2020, Sartorius launched BIOSTAT STR Generation 3 single-use bioreactor and BIOBRAIN automation platform to introduce innovations that will change the field of biopharmaceutical process development and manufacturing. Biostat STR simplifies biologics production.

Company Profiles

- Merck KGaA

- Sartorius AG

- Thermo Fisher Scientific Inc

- Corning Inc

- STAMM Biotech

- Lonza Group AG

- Eppendorf SE

- Repligen Corp

- Danaher Corp

- BioPharma Dynamics Ltd

Report Coverage

Revenue forecast, Company Analysis, Industry landscape, Growth factors, and Trends

Segment Covered

Type, Modality, and End User

Regional Scope

North America, Europe, Asia Pacific, Middle East & Africa, South & Central America

Country Scope

Argentina, Australia, Brazil, Canada, China, France, Germany, India, Italy, Japan, Mexico, Saudi Arabia, South Africa, South Korea, Spain, United Arab Emirates, United Kingdom, United States

Frequently Asked Questions

Bioprocessing is the process that utilizes complete living cells or components (e.g., bacteria, enzymes, and proteins) to obtain desired products. The process is commonly known as fermentation. The entire process is divided into three stages: upstream process, fermentation, and downstream process. The upstream process involves preparation of liquid media, separation of particulate and inhibitory chemicals through sterilization and air purification. Additionally, fermentation involves the conversion of substrate to obtain desired products through biological agents such as microorganisms. Furthermore, downstream processing involves separation of cells from the fermentation broth, purification and concentration of desired products and waste disposal or recycle method.

The growing R&D spendings to introduce new drug compounds, and increasing prevalence of chronic diseases. However, stringent regulatory policies are restricting the market growth.

Based on type, cell culture media bioprocess took the forefront leaders in the worldwide market by accounting largest share in 2022 and is expected to continue to do so till the forecast period.

Global bioprocess technology market is segmented by region into North America, Europe, Asia Pacific, the Middle East & Africa, and South & Central America. In North America, the U.S. held the largest market share for bioprocess technology market. The US is expected to hold the largest share in the bioprocess technology market during the forecast period. The presence of top players and favorable regulations related to product approvals coupled with commercializing new products are the contributing factors for the regional growth. Additionally, the increasing number of technological advancements is the key factor responsible for the Asia Pacific regional growth in the coming years.

Merck KGaA, Sartorius AG, Thermo Fisher Scientific Inc, Corning Inc, STAMM Biotech, Lonza Group AG, Eppendorf SE, Repligen Corp, Danaher Corp, BioPharma Dynamics Ltd; are among the leading companies operating in the global bioprocess technology market

The single use segment dominated the global bioprocess technology market.

The List of Companies - Bioprocess Technology Market

- Merck KGaA

- Sartorius AG

- Thermo Fisher Scientific Inc

- Corning Inc

- STAMM Biotech

- Lonza Group AG

- Eppendorf SE

- Repligen Corp

- Danaher Corp

- BioPharma Dynamics Ltd

The Insight Partners performs research in 4 major stages: Data Collection & Secondary Research, Primary Research, Data Analysis and Data Triangulation & Final Review.

- Data Collection and Secondary Research:

As a market research and consulting firm operating from a decade, we have published many reports and advised several clients across the globe. First step for any study will start with an assessment of currently available data and insights from existing reports. Further, historical and current market information is collected from Investor Presentations, Annual Reports, SEC Filings, etc., and other information related to company’s performance and market positioning are gathered from Paid Databases (Factiva, Hoovers, and Reuters) and various other publications available in public domain.

Several associations trade associates, technical forums, institutes, societies and organizations are accessed to gain technical as well as market related insights through their publications such as research papers, blogs and press releases related to the studies are referred to get cues about the market. Further, white papers, journals, magazines, and other news articles published in the last 3 years are scrutinized and analyzed to understand the current market trends.

- Primary Research:

The primarily interview analysis comprise of data obtained from industry participants interview and answers to survey questions gathered by in-house primary team.

For primary research, interviews are conducted with industry experts/CEOs/Marketing Managers/Sales Managers/VPs/Subject Matter Experts from both demand and supply side to get a 360-degree view of the market. The primary team conducts several interviews based on the complexity of the markets to understand the various market trends and dynamics which makes research more credible and precise.

A typical research interview fulfils the following functions:

- Provides first-hand information on the market size, market trends, growth trends, competitive landscape, and outlook

- Validates and strengthens in-house secondary research findings

- Develops the analysis team’s expertise and market understanding

Primary research involves email interactions and telephone interviews for each market, category, segment, and sub-segment across geographies. The participants who typically take part in such a process include, but are not limited to:

- Industry participants: VPs, business development managers, market intelligence managers and national sales managers

- Outside experts: Valuation experts, research analysts and key opinion leaders specializing in the electronics and semiconductor industry.

Below is the breakup of our primary respondents by company, designation, and region:

Once we receive the confirmation from primary research sources or primary respondents, we finalize the base year market estimation and forecast the data as per the macroeconomic and microeconomic factors assessed during data collection.

- Data Analysis:

Once data is validated through both secondary as well as primary respondents, we finalize the market estimations by hypothesis formulation and factor analysis at regional and country level.

- 3.1 Macro-Economic Factor Analysis:

We analyse macroeconomic indicators such the gross domestic product (GDP), increase in the demand for goods and services across industries, technological advancement, regional economic growth, governmental policies, the influence of COVID-19, PEST analysis, and other aspects. This analysis aids in setting benchmarks for various nations/regions and approximating market splits. Additionally, the general trend of the aforementioned components aid in determining the market's development possibilities.

- 3.2 Country Level Data:

Various factors that are especially aligned to the country are taken into account to determine the market size for a certain area and country, including the presence of vendors, such as headquarters and offices, the country's GDP, demand patterns, and industry growth. To comprehend the market dynamics for the nation, a number of growth variables, inhibitors, application areas, and current market trends are researched. The aforementioned elements aid in determining the country's overall market's growth potential.

- 3.3 Company Profile:

The “Table of Contents” is formulated by listing and analyzing more than 25 - 30 companies operating in the market ecosystem across geographies. However, we profile only 10 companies as a standard practice in our syndicate reports. These 10 companies comprise leading, emerging, and regional players. Nonetheless, our analysis is not restricted to the 10 listed companies, we also analyze other companies present in the market to develop a holistic view and understand the prevailing trends. The “Company Profiles” section in the report covers key facts, business description, products & services, financial information, SWOT analysis, and key developments. The financial information presented is extracted from the annual reports and official documents of the publicly listed companies. Upon collecting the information for the sections of respective companies, we verify them via various primary sources and then compile the data in respective company profiles. The company level information helps us in deriving the base number as well as in forecasting the market size.

- 3.4 Developing Base Number:

Aggregation of sales statistics (2020-2022) and macro-economic factor, and other secondary and primary research insights are utilized to arrive at base number and related market shares for 2022. The data gaps are identified in this step and relevant market data is analyzed, collected from paid primary interviews or databases. On finalizing the base year market size, forecasts are developed on the basis of macro-economic, industry and market growth factors and company level analysis.

- Data Triangulation and Final Review:

The market findings and base year market size calculations are validated from supply as well as demand side. Demand side validations are based on macro-economic factor analysis and benchmarks for respective regions and countries. In case of supply side validations, revenues of major companies are estimated (in case not available) based on industry benchmark, approximate number of employees, product portfolio, and primary interviews revenues are gathered. Further revenue from target product/service segment is assessed to avoid overshooting of market statistics. In case of heavy deviations between supply and demand side values, all thes steps are repeated to achieve synchronization.

We follow an iterative model, wherein we share our research findings with Subject Matter Experts (SME’s) and Key Opinion Leaders (KOLs) until consensus view of the market is not formulated – this model negates any drastic deviation in the opinions of experts. Only validated and universally acceptable research findings are quoted in our reports.

We have important check points that we use to validate our research findings – which we call – data triangulation, where we validate the information, we generate from secondary sources with primary interviews and then we re-validate with our internal data bases and Subject matter experts. This comprehensive model enables us to deliver high quality, reliable data in shortest possible time.

Trends and growth analysis reports related to Bioprocess Technology Market

Jun 2023

Wound Closure Devices Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Sutures, Adhesives, Staplers, Strips, and Others), Wound Type (Chronic Wound and Acute Wound), End User (Hospitals, Clinics, Ambulatory Surgery Centers, and Others), and Geography

Jun 2023

Pediatric Cardiology Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product Type (Transcatheter Heart Valves, Occlusion Devices, Catheters, Stents, Introducer Sheaths, and Others), Disease Indication (Congenital Heart Disease, Acquired Heart Disease, Arrhythmias, Cardiomyopathies, and Others), Surgical Procedure (Interventional Procedures, Heart Rhythm Management Procedures, and Others), End User (Hospitals, Specialty Clinics, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Jun 2023

Pharmaceutical Membrane Filters Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Technology (Microfiltration, Ultrafiltration, Reverse Osmosis and Nanofiltration), Design (Hollow Fiber, Spiral Wound, Tubular System and Plate and Frame), Material (Polyethersulfone (PES), Polysulfone (PS), Cellulose-Based Membranes, Polytetrafluoroethylene (PTFE), Polyvinyl Chloride (PVC), Polyacrylonitrile (PAN) and Others), End User (Pharmaceutical and Biotech Industries and CROs and CDMOs), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South & Central America)

Jun 2023

ECG Devices Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Resting ECG and Stress ECG), Lead Type (12-Lead ECG, 3–6 Lead ECG, and Single Lead), Technology [Portable (Wired) ECG System and Wireless ECG System], End User (Hospital and Clinics, Ambulatory Surgical Centers, Cardiac Centers, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South & Central America)

Jun 2023

Surgical Laser Fiber Units Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (CO2 Laser, Diode Laser, Erbium Laser, Nd:YAG Laser, Holmium Laser, Alexandrite Laser, and Others), Material (Silica-Based Fibers, Quartz Fibers, Polymer-Based Fibers, Multimode Fibers, and Others), Power (Low-Power Lasers, Medium-Power Lasers, and High-Power Lasers), Application (Urology, Dermatology, Gynecology, Cardiology, Neurology, Ophthalmology, Respiratory, Dentistry and Others), Wavelength (9,301 nm and above, 2,941–9,300 nm, and 1,441–2,940 nm, 821–1,440 nm, 710–820 nm, and below 710 nm), End User (Hospitals, Specialty Clinics, Physician Office, and Others), and Geography

Jun 2023

Therapeutic Vaccines Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Product (Cancer Vaccines, Infectious Disease Vaccines, and Others), Technology (Allogenic Vaccines and Autologous Vaccines), End User (Hospitals, Clinics, and Others), and Geography

Jun 2023

Medical Cables Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Type (Disposable Medical Cables, Reusable Medical Cables, and Custom Medical Cables), Applications [Diagnostics (Ultrasound Cables, Endoscopy Cables, Patient Interface Cables, and Others), Motorized Equipment, Patient Monitoring (ECG Cables, SpO2 Cables, NiBP Cables, EEG Cables, and Others), Surgical and Life Support (Fiber Optics, Modular Local Area Network, and Others), and Others], End User (Hospital and Clinics, Diagnostic Laboratories and Imaging Centers, Ambulatory Surgical Centers, and Others), and Geography

Jun 2023

Laser-Assisted ENT Surgeries Market

Size and Forecast (2021 - 2031), Global and Regional Share, Trend, and Growth Opportunity Analysis Report Coverage: By Laser Type (C02 Laser, Nd:YAG Laser, Diode Laser, Blue Laser, KTP Laser, Argon Laser, and Other Laser Types), Surgery Type [Laser Laryngeal Surgery, Laser Endoscopic Sinus Surgery (LESS), Laser-Assisted Uvulopalatoplasty (LAUP), Laser-Assisted Stapedotomy, Laser-Assisted Tonsillectomy and Adenoidectomy, Laser Turbinates Reduction, Transoral Laser Microsurgery (TLM), Nasal Surgery, and Other Surgery Types], End User (Hospitals and Specialty Clinics, Physician Offices, and Other End Users), and Geography (North America, Europe, Asia Pacific, South and Central America, and Middle East and Africa)